Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

EFAMA’s Reply to LEI ROC’s 2nd Consultation Document on Fund Relationships in the Global LEI System

EFAMA response to EMMI's 2nd consultation on a new hybrid methodology for Euribor

EFAMA reply to FSB consultation on Incentives to Centrally Clear over-the-Counter (OTC) Derivatives

EU Equity Consolidated Tape Proposal - Statement of Principles

A Cross-Industry Consensus on the EU Equity Consolidated Tape Proposal - Statement of Principles

EFAMA, AFME, BVI and Cboe agreed on a set of 11 Principles.

The provision of an appropriately constructed EU Equities Consolidated Tape (“CT”) will democratise access to equities (as proposed by the EU Commission) for all investors, regardless of resources or sophistication, with a comprehensive and standardised view of EU equities prices.

EFAMA’s reply to ESMA’s consultation paper on the opinion on Trading Venue Perimeter

We welcome this opportunity to comment on a review of the TV perimeter, and support ESMA’s objective of clarifying when systems and facilities qualify as multilateral.

EFAMA views and recommendations on ESMA's consultation on the review of EMIR RTS on APC margin measures

The European Fund and Asset Management Association (EFAMA) welcomes the opportunity to respond to this important review of RTS 153/2013 and accompanying guidelines, in light of the procyclicality witnessed during the peak volatility of the Covid crisis. European CCPs already have standard anti-procyclicality tools in their rulebooks and this did lead to less volatile moves in margin in Europe versus other jurisdictions.

Household Participation in Capital Markets

This report analyses the progress made in recent years by European households in allocating more of their financial wealth to capital market instruments (pension plans, life insurance, investment funds, debt securities and listed shares) and less in cash and bank deposits. It also includes policy recommendations on improving retail participation in capital markets, including for the Retail Investment Strategy currently under discussion.

Some key findings include:

Buy-side use-cases for a real-time consolidated tape

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

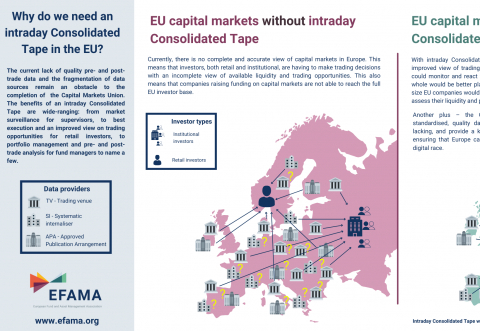

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.