We appreciate the opportunity to respond to this important consultation and remain gladly at the disposal of the European Commission staff to elaborate on any of our responses.

Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

Related policy positions

Policy position

Capital Markets

15 December 2016

EFAMA Position on the draft Joint Guidelines of ESAs regarding customer due diligence under Anti-Money Laundering Directive

EFAMA is closely monitoring the recent regulatory developments in the field of anti-money laundering and counter-terrorist financing, in particular the due diligence duties of the asset management sector. EFAMA is embracing the objective of enhancing transparency and accessibility to the beneficial ownership information and also fully acknowledges the importance of obtaining accurate identification and verification data of natural and legal persons for fighting money laundering and terrorist financing.

Policy position

Capital Markets

Data

Distribution & Client Disclosures

05 December 2016

EFAMA's reply to ESMA's CP on RTS specifying the scope of the consolidated tape for non-equity financial instruments

EFAMA supports every efforts made to enhance financial markets regulation which reinforces the stability and the transparency of the financial system.

In that perspective, EFAMA welcomes the opportunity to comment on the ESMA Consultation Paper on RTS specifying the scope of the consolidated tape for non-equity financial instruments. We consider that a consolidate tape (“CT”) is a key positive factor for price formation and transparency.

Prior to replying to the consultation, we wish to make the following general remarks

Related news

Announcement

Capital Markets

Capital Markets Union

Competitiveness

EU Fund regulation

International agenda

Investor Education

Management Companies

Sustainable Finance

Tax & Accounting

10 November 2021

Thank you to the Investment Management Forum sponsors | Register now!

Register now for our Investment Management Forum next week! High-calibre panels and keynote speakers promise rich, informative and thought-provoking exchanges between European policymakers, investment managers and regulators on

- the Competitiveness of our industry

- the EU retail investment strategy

- the latest in global standards for sustainability reporting

- challenges and opportunities of alternative investment regulations

- the impact of digitalisation on asset management

- and more...

Press Release

Capital Markets

EMIR

MIFID

Capital Markets Union

Data

07 October 2021

Statement on the release of the Oliver Wyman study ‘Caught on Tape’

“Oliver Wyman’s study ‘Caught on Tape’ provides a perplexing take on Consolidated Tape for Europe. Sure enough, it starts with accurate observations: the high number of trading venues in Europe, the resultant fragmented liquidity, unseen liquidity due to the lack of a consolidated tape, and the fact that leading markets like the US and Canada today benefit from a real time consolidated tape.

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

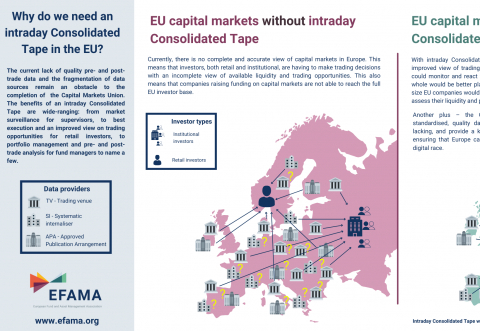

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Related publications

Publication

Capital Markets

MIFID

Data

Distribution & Client Disclosures

04 March 2020

3 Questions to Rudolf Siebel on Market Data Costs

Q #1 Have you witnessed an increase in the cost of market data over the last couple of years? If so, how can it be explained?

Publication

Capital Markets

Capital Markets Union

Competitiveness

EU Fund regulation

International agenda

Management Companies

Sustainable Finance

Tax & Accounting

17 September 2019

Asset Management Report 2019

The EFAMA Asset Management in Europe report aims at providing facts and figures to gain a better understanding of the role of the European asset management industry. It takes a different approach from that of the other EFAMA research reports, on two grounds. Firstly, this report does not focus exclusively on investment funds, but it also analyses the assets that are managed by asset managers under the form of discretionary mandates. Secondly, the report focuses on the countries where the investment fund assets are managed rather than on the countries in which the funds are domiciled.

Publication

Capital Markets

Capital Markets Union

Competitiveness

Distribution & Client Disclosures

EU Fund regulation

Management Companies

Sustainable Finance

24 September 2018

Asset Management Report 2018

Contact

Deputy Director, Capital Markets and Digital