Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

EFAMA responds to EC draft DA on integration of ESG into MiFID II

EFAMA's reply to ESMA CP on Technical standards on reporting, data quality, data access & registration of Trade Repositories under EMIR REFIT

EFAMA's reply to ESMA's CP on PTRR services with regards to the clearing obligation

Joint association letter on the CSDR Settlement Discipline implementation timeline

On 14 July 2021, sixteen trade associations, representing buy-side, sell-side and market infrastructures, wrote to ESMA and the European Commission regarding the timeline for implementation of the mandatory buy-in rules as part of the CSDR Settlement Discipline Regime.

The Joint Associations welcome the Report from the Commission on the CSDR Review published in July 2021 and fully support the Commission’s intention to consider amendments to the mandatory buy-in regime, subject to an impact assessment.

Ensuring a market structure and a transparency regime which facilitate liquidity, investors’ choice, and funding of companies | Joint statement

Well-functioning and liquid capital markets are fostered by an efficient market structure and supporting legislative frameworks. A diverse and efficient market structure reduces the costs of trading whilst promoting best execution. This optimises funding opportunities for issuers and maximises returns for investors and savers.

3 Questions to Jean-Louis Schirmann on the use of EURIBOR

Q #1 How was Euribor impacted by the adoption of the Benchmark Regulation (BMR) and what are the relevant features of the reformed Euribor for investment managers?

Household Participation in Capital Markets

This report analyses the progress made in recent years by European households in allocating more of their financial wealth to capital market instruments (pension plans, life insurance, investment funds, debt securities and listed shares) and less in cash and bank deposits. It also includes policy recommendations on improving retail participation in capital markets, including for the Retail Investment Strategy currently under discussion.

Some key findings include:

Buy-side use-cases for a real-time consolidated tape

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

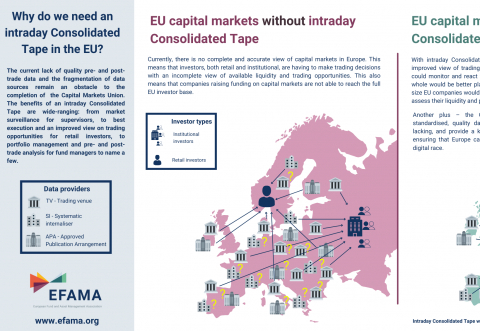

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.