Capital Markets Union

Building a Capital Markets Union (CMU) serving the needs of European citizens and businesses is as ambitious as it is essential: the effort will enable pensioners and savers to share in the upside of Europe’s economic recovery. In the process, European capital markets also become more efficient and better integrated. This long-term vision is key to financing European innovation and to supporting the transition towards a more sustainable economy.

Increasing retail investors’ participation in capital markets is an essential component for building an effective CMU. Improving access to financial and non-financial information and addressing the high data costs our industry is encountering, are also important steps towards a functioning CMU. All this, while maintaining and improving the attractiveness of the European investment management sector in today's global environment.

EFAMA prepared a list of key actions that are required to reach the CMU objectives from an investor perspective. We have also developed a specific Key Performance Indicator to measure year-on-year progress towards increasing retail participation in capital markets in each member state.

Joint EU Trade Associations' views on ‘Review of the European System of Financial Supervision’

EFAMA on EC Proposal on low-carbon benchmarks and positive carbon impact benchmarks

EFAMA comments European Commission's Proposal on disclosures relating to sustainable investments

Annual European Asset Management Report - Report highlights key developments in the European fund industry

The European Fund and Asset Management Association (EFAMA) has released the 13th edition of its Asset Management in Europe report, which provides in-depth analysis of recent trends in the European asset management industry, focussing on where investment funds and discretionary mandates are managed in Europe.

IMF 2021: Thought-provoking discussions and insightful presentations

This year’s Investment Management Forum featured an incredible number of high-level speakers and thought-provoking discussions.

.png)

EFAMA welcomes proposal on affordable consolidated tape - The association continues to urge action on market data costs

EFAMA is pleased to read today the details of a robust MiFIR proposal from the European Commission addressing key areas of reform around the creation of a consolidated tape (CT), along with adjustments to transparency requirements on trading.

Household Participation in Capital Markets

This report analyses the progress made in recent years by European households in allocating more of their financial wealth to capital market instruments (pension plans, life insurance, investment funds, debt securities and listed shares) and less in cash and bank deposits. It also includes policy recommendations on improving retail participation in capital markets, including for the Retail Investment Strategy currently under discussion.

Some key findings include:

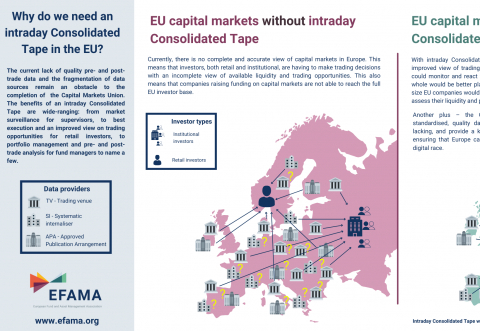

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Market Insights | Issue #5 | Perspective on the net performance of UCITS

Equity UCITS delivered a total net return of 108% in real terms in 2010-2019, whereas bank deposits lost 10% in net value