EFAMA is pleased to read today the details of a robust MiFIR proposal from the European Commission addressing key areas of reform around the creation of a consolidated tape (CT), along with adjustments to transparency requirements on trading.

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

EFAMA is pleased to read today the details of a robust MiFIR proposal from the European Commission addressing key areas of reform around the creation of a consolidated tape (CT), along with adjustments to transparency requirements on trading.

EFAMA welcomes this opportunity to comment on the review of the provisions within the Short Selling Regulation. We have limited our responses to those questions of most relevance to our membership.

Nine associations (AFME, AIMA, EAPB, EBF, EFAMA, FIA, ICI, ISDA, SIFMA AMG) welcome the Commission's decision to grant a time-limited equivalence decision in respect of UK CCPs. However, when this time-limited equivalence decision expires on 30 June 2022, there remains a significant risk of disruption to clearing for EU firms and to their access to global markets.

EFAMA is pleased to share the link to the educational webinar it organised on 14 June with leading buy-side clearing experts, including Allianz Global Investors, Aviva Investors, BlackRock and Nordea Asset Management, to discuss the main findings of EFAMA's recent analysis on mandated active accounts for EU clearing.

European asset managers continue to urge policymakers to support the European Parliament’s proposal for an Equities/ETFs consolidated tape which includes 5 layers of real-time pre-trade data. Market participants, including the European buy and sell-sides have consistently maintained that a post-trade only equities/ETFs consolidated tape will not meet with the market demand required to make the tape commercially viable. Tanguy van de Werve, Director General of EFAMA, stated: “This would be a legislative se

EFAMA welcomes the recent proposal by European exchanges to build a consolidated tape. This affirms the buy-side’s long standing view that a European consolidated tape is key to completing the objectives of the Capital Markets Union and ensuring that European capital markets remain globally competitive. We have identified important use-cases for institutional and retail investors alike, not least in the ability to receive best execution on trades.

This report analyses the progress made in recent years by European households in allocating more of their financial wealth to capital market instruments (pension plans, life insurance, investment funds, debt securities and listed shares) and less in cash and bank deposits. It also includes policy recommendations on improving retail participation in capital markets, including for the Retail Investment Strategy currently under discussion.

Some key findings include:

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

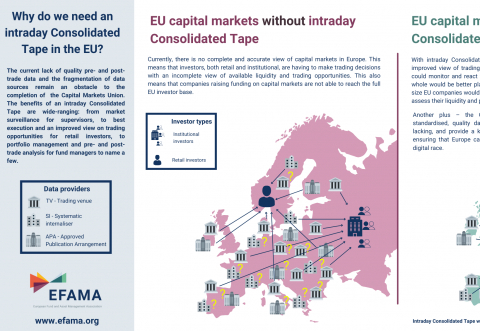

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.