EFAMA supports the European Commission's initiative to establish the European Single Access Point. We see it as a unique opportunity for the Capital Markets Union to centralise all publicly available ESG and financial transparency information data in one place.

Data

In the modern economy, data is increasingly becoming a strategic asset. This is particularly true for the asset management industry, where data forms the backbone of the daily activities and internal processes necessary to guarantee best practices in portfolio management.

Asset managers are major users of a variety of data, including market data, index data and, increasingly, ESG data. EFAMA advocates for, and seeks to support members’ access to, high-quality, standardised and comparable data at a fair price. EFAMA also encourages the creation of a well-structured, reasonably priced consolidated tape fed by all trading venues and systematic internalisers for all financial instruments.

Related policy positions

Policy position

Capital Markets Union

Data

Sustainable Finance

12 March 2021

EFAMA response to Commission consultation on establishment of European Single Access Point (ESAP)

Policy position

Data

International agenda

01 March 2021

EFAMA responds to IOSCO Consultation on Market Data in Secondary Equity Market

EFAMA supports the initiatives launched by IOSCO and other regulators (e.g. ESMA, FCA, SEC) to analyse and address the significant issues concerning market data in the secondary equity market.

Policy position

Data

11 January 2021

EFAMA's reply to ESMA's CP on the Guidelines on the MiFID II / MiFIR Obligations on Market Data

EFAMA welcomes this ESMA initiative and we agree with the conclusions in the ESMA Report that there is an overall need to strengthen the laws applicable to data in connection with the MiFIDII/MiFIR Review, aside the implementation of a Consolidated Tape . We consider that the draft Guidelines will further strengthen the MiFID level 1 and level 2 measures and will foster the establishment of a cost-based approach for market data procurement. Therefore, we would be in favour of turning the proposed guidelines into binding regulation.

Related news

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

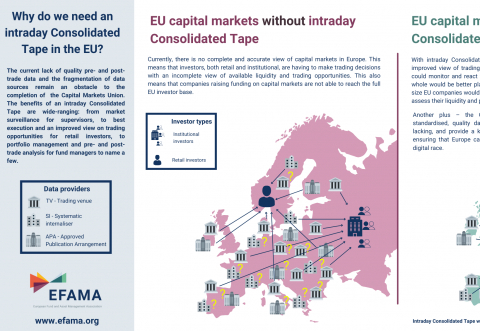

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Publication

Competitiveness

Data

EU Fund regulation

Exchange-traded Funds

Money Market Funds

UCITS

Management Companies

AIFMD

Statistics

Sustainable Finance

01 July 2021

EFAMA publishes 2021 industry Fact Book - Report highlights key developments in the European fund industry in 2020

EFAMA has released its 2021 industry Fact Book.

The 2021 Fact Book provides an in-depth analysis of trends in the European fund industry, an extensive overview of the regulatory developments across 29 European countries and a wealth of data.

Policy Position

Capital Markets

Data

14 June 2021

Joint statement by EFAMA and EFSA on Consolidated Tape and market data costs

The appropriate construction, and conditions for the usage, of a Consolidated Tape

Related publications

Publication

Data

EU Fund regulation

29 June 2020

Global Memo on Market Data Costs

In a report released today, the International Council of Securities Associations (ICSA), the European Fund and Asset Management Association (EFAMA), and the Managed Funds Association (MFA) call for the implementation of internationally recognized principles to address excessively high market data fees and unfair licensing provisions.

Publication

Capital Markets

Capital Markets Union

Competitiveness

Data

Distribution & Client Disclosures

EU Fund regulation

International agenda

Management Companies

Pensions

Stewardship

Supervision

Sustainable Finance

Tax & Accounting

11 June 2020

Annual Review June 2019-June 2020

"It gives me great pleasure to provide you with an overview of our activities since our Annual General Meeting in Paris last year. While we were very much looking forward to hosting you all in Brussels this week, the current crisis and associated travel restrictions has forced us to improvise and turn our meeting into a virtual AGM.

Publication

Capital Markets Union

Competitiveness

Data

EU Fund regulation

UCITS

International agenda

27 May 2020

EFAMA Market Insights | Issue #1 | Net outflows from UCITS in March 2020 - Industry weathers Covid-19 crisis

The Covid-19 pandemic significantly impacted financial markets. Stock markets across the world suffered a steep decline driven by lower economic growth and corporate profits. As anticipated, the crisis caused substantial net outflows from UCITS in March (EUR 313 billion). However, as a percentage of net assets, these outflows were no higher than in October 2008, at the height of the global financial crisis (2.9%).

Contact

Deputy Director, Capital Markets and Digital