The European Commission’s proposal on MiFIR establishes the blueprint for a consolidated tape (CT) for Europe’s capital markets. It also significantly alters the competitive market structure brought about by MiFID II by introducing greater transparency requirements. Finally, it addresses important issues around market data costs.

Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

Related policy positions

Policy position

Capital Markets

MIFID

14 February 2022

EFAMA position MiFIR review - a buy-side view on consolidated and market structure reforms

Policy position

Capital Markets

27 January 2022

IOSCO Consultation on 'Review of margining practices'

We commend the work that IOSCO has undertaken to date on this topic including the survey work and the summary findings in the form of the report currently under review. It is fair to say that the conclusions of the report and areas for further work gave rise to detailed discussions within our industry, yielding ultimately firm views on the priority areas that we support and see value in, and areas we felt were not reflected in the study and thereby building risk into margining models in future crisis scenarios. These areas are fur

Policy position

Capital Markets

EMIR

24 January 2022

ESMA consultation on the review of clearing thresholds under EMIR

For asset managers the main issue continues to be the reclassification of ETDs as OTCs as a result of the non-equivalence of UK regulated markets. While we understand that a review is legally mandated at this point in time, we do not see value in recalibrating the various thresholds or making changes to the calculation methodologies unless these are in the two areas we define below. Our main concern revolves around the fact that changes would carry significant compliance costs while making little impact on the population of counterparties and notional captured by the thresholds.

Related news

Press Release

Capital Markets

EMIR

MIFID

Capital Markets Union

Data

07 October 2021

Statement on the release of the Oliver Wyman study ‘Caught on Tape’

“Oliver Wyman’s study ‘Caught on Tape’ provides a perplexing take on Consolidated Tape for Europe. Sure enough, it starts with accurate observations: the high number of trading venues in Europe, the resultant fragmented liquidity, unseen liquidity due to the lack of a consolidated tape, and the fact that leading markets like the US and Canada today benefit from a real time consolidated tape.

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

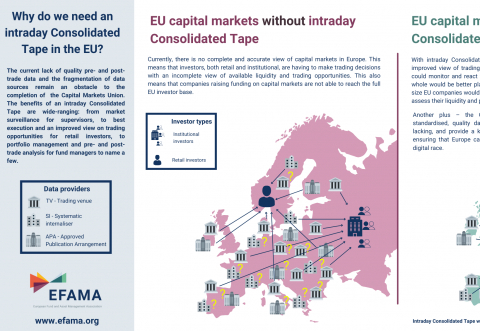

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Policy Position

Capital Markets

EMIR

16 September 2021

UK clearing house equivalence - request from nine trade associations

Nine associations (AFME, AIMA, EAPB, EBF, EFAMA, FIA, ICI, ISDA, SIFMA AMG) welcome the Commission's decision to grant a time-limited equivalence decision in respect of UK CCPs. However, when this time-limited equivalence decision expires on 30 June 2022, there remains a significant risk of disruption to clearing for EU firms and to their access to global markets.

Related publications

Publication

Capital Markets

01 July 2025

Advancing EU capital markets: Prioritising key targets for the Savings and Investments Union

Publication

Capital Markets

Capital Markets Union

Retail Investment

22 January 2024

Household Participation in Capital Markets

This report analyses the progress made in recent years by European households in allocating more of their financial wealth to capital market instruments (pension plans, life insurance, investment funds, debt securities and listed shares) and less in cash and bank deposits. It also includes policy recommendations on improving retail participation in capital markets, including for the Retail Investment Strategy currently under discussion.

Some key findings include:

Publication

Capital Markets

MIFID

16 November 2021

Buy-side use-cases for a real-time consolidated tape

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

Contact

Deputy Director, Capital Markets and Digital