We welcome this opportunity to comment on a review of the TV perimeter, and support ESMA’s objective of clarifying when systems and facilities qualify as multilateral.

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

We welcome this opportunity to comment on a review of the TV perimeter, and support ESMA’s objective of clarifying when systems and facilities qualify as multilateral.

EFAMA welcomes the opportunity to respond to the EC’s targeted consultation on the EU’s central clearing framework. We are pleased to find in this consultation document a fair reflection of the complexity of the CCP ecosystem and consistency with the issues raised in previous dialogues held with the European Commission. In that same spirit, we hope in our response to provide feedback that resonates with the EC’s broader policy objectives while minimizing systemic risk and undue harm to our industry.

The European Fund and Asset Management Association (EFAMA) welcomes the opportunity to respond to this important review of RTS 153/2013 and accompanying guidelines, in light of the procyclicality witnessed during the peak volatility of the Covid crisis. European CCPs already have standard anti-procyclicality tools in their rulebooks and this did lead to less volatile moves in margin in Europe versus other jurisdictions.

We welcome this opportunity to comment on a review of the TV perimeter, and support ESMA’s objective of clarifying when systems and facilities qualify as multilateral.

The European Fund and Asset Management Association (EFAMA) welcomes the opportunity to respond to this important review of RTS 153/2013 and accompanying guidelines, in light of the procyclicality witnessed during the peak volatility of the Covid crisis. European CCPs already have standard anti-procyclicality tools in their rulebooks and this did lead to less volatile moves in margin in Europe versus other jurisdictions.

The European Fund and Asset Management Association (EFAMA) has today published its position paper on the European Commission’s proposed Markets in Financial Instruments Regulation review which establishes a blueprint for a consolidated tape (CT) across Europe’s capital markets.

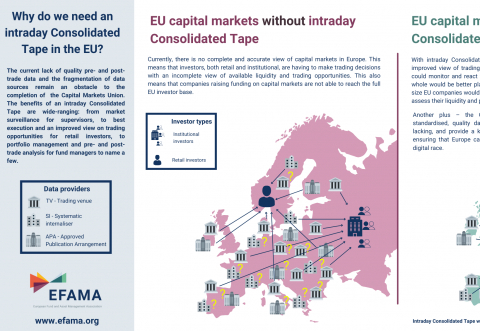

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

The London Interbank Offered Rate, also known as LIBOR®, is a widely-used index for short-term interest rates that is commonly found in